Main Street Monday — Differences in Small Bank vs Large Bank Small Business Lending Data Collection

November 25, 2024

Bob Coleman

Founder & Publisher

Main Street Monday — Differences in Small Bank vs Large Bank Small Business Lending Data Collection

From the FDIC October 2024 Small Business Lending Survey – See HERE

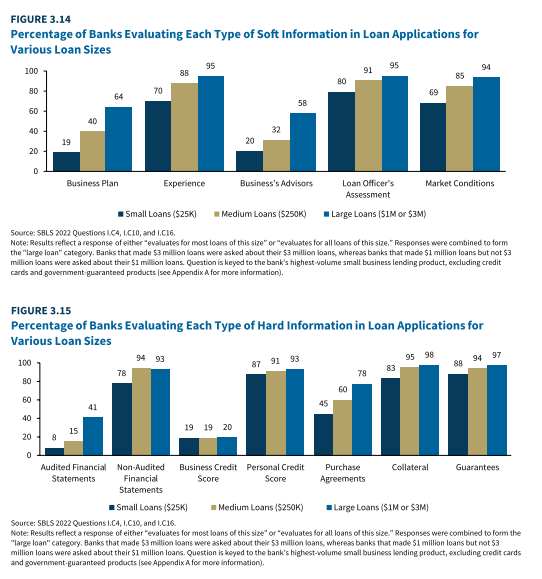

While banks use various methods to assess small businesses, small and large banks are believed to have distinct advantages in processing information. This leads to differences in how they manage their small business lending programs.

Small banks excel at gathering and using “soft” information, which is difficult to quantify or communicate. They obtain this information through direct, repeated interactions with potential borrowers and knowledge of the local community. The close-knit structure of small banks, with few managerial layers between owners and loan officers, may motivate officers to gather and use soft information when making lending decisions.

Additionally, small banks’ local presence reduces the cost of building relationships with firms and understanding the local market. This flexibility allows small banks to address credit needs on a case-by-case basis, earning them the label of “relationship lenders.”

Large banks leverage economies of scale to collect and utilize large amounts of quantifiable, or “hard,” information about current and potential borrowers. This approach requires bank management to predetermine the types of data and metrics used to assess small business quality. Consequently, large banks’ lending decisions are more likely to be based on financial variables. The quantifiable nature of this information allows for electronic submission and sharing, reducing the need for decision-makers to be in close proximity to the small business. This high-volume lending model is often referred to as “transactional lending.”

However, the use of different information processing models does not necessarily mean banks will employ different strategies when interacting with small business borrowers. As noted in the 2016 Small Business Lending Survey report (FDIC 2018), a high-touch, staff-intensive approach to customer relationships does not always indicate that a bank emphasizes soft information in its underwriting. Similarly, the adoption of consumer-facing technology like mobile apps does not necessarily imply a more transactional approach to credit decisions, though banks may incorporate data gathered through these interactions into their underwriting process. In fact, certain effective practices for building and maintaining relationships with small business customers are nearly universal in banking, even if banks differ in how those relationships influence credit decision-making.