Are SBA Loans Bad for the Economy?

October 8, 2014

By Bob Coleman

Editor, Coleman Report

Asks our friend Kent Hoover while covering a report issued by the National Bureau of Economic Research.

Asks our friend Kent Hoover while covering a report issued by the National Bureau of Economic Research.

Their conclusion?

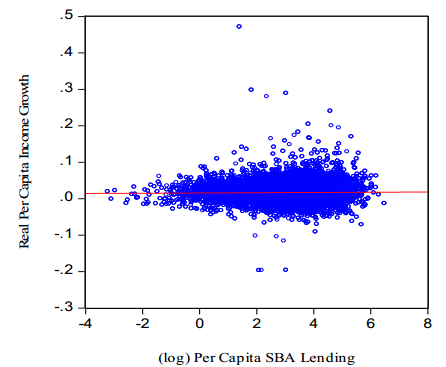

“A spatial econometric analysis suggests than an increase in SBA loans per capita in a county is associated with negative effects on its own rate of income; also the growth rates of neighboring counties.”

Say what?

Overall, a 10 percent increase in SBA loans per capita is associated with a cumulative decrease in income growth rates of about 2 percent,” the researchers found.

That could be because “SBA lending to small businesses comes at the cost of loans that would have otherwise been made to more profitable and/or innovative firms,” they conclude.

This hit piece is another constant reminder that the industry needs to be ahead of the argument that SBA lending programs pay for themselves and support Main Street to create jobs. Of course, the tax revenue (sales tax by the consumer, payroll tax by the small business owner, income tax by the employee) generated by SBA loan job creation are always ignored in these type of reports.

Glancing at the report I already know the fallacies. 1) There was this event called the great recession that will skew all numbers. 2) Comparing urban counties with adjoining rural counties is comparing apples to oranges. Urban economies always trump rural economies. To suggest an increase in Los Angeles county SBA lending is a detriment to Riverside and San Bernardino county economy’s is laughable. Riverside and San Bernardino suffered from the recession and falling real estate values, not from LA county SBA lending. 3) Researchers who issue complex reports with multi-syllable words that no one understands are obfuscating their findings with psycho babble.

Their conclusion is political and self-serving.

The true question is, “How much worse would the economies of America’s rural counties be without SBA and USDA rural lending programs?”